7% return from SIP. This line might make you wonder why I did not quit my SIP and choose another investment option.

After all, even a PPF account pays more than that. So why should anyone continue investing in mutual funds through SIPs?

What is the logic behind it?

I know many newcomers might be confused—whether I am promoting SIPs or criticizing them so that others don’t fall prey to blind investing.

And I also know you didn’t expect such a post from me.

If you have read my evergreen post on how I reached a ₹1 crore portfolio by starting my investing journey with just ₹500, this might feel even more confusing.

But the truth—and the real logic—lies in the paragraphs below.

Did a 7% return from my SIP trigger any action from me? Let’s break it down below.

Did a 7% SIP Return Really Mean Failure?

Yes, it is a failure if I consistently get only 7% returns from my SIPs. SIPs invest in mutual funds, and mutual funds are equity-related products.

Equity products are volatile and risky by nature. So the question is valid—why should I stay invested if I am taking risk and getting only a 7% return?

Especially when such returns are possible through relatively risk-free investments like PPF or even some FDs.

But this is where the real meaning comes in.

This is what consistency looks like. Monthly fluctuations. Zero panic. SIPs continued. +7% in 2025.

Why Comparing SIP Returns With PPF Is Misleading

I cannot compare my SIP returns with PPF, and the reason is simple. PPF has a fixed interest rate, and these rates rarely change.

Expecting returns higher than 7%—or returns equivalent to equity products—from PPF in the long run is close to impossible. You simply can’t expect 12% returns from PPF.

With SIPs, however, I can at least expect inflation-beating returns over the long term.

If I look at my long-term mutual fund performance, it is far higher than 7%.

In fact, even my lowest-performing mutual fund has delivered over 13.5% returns in the last 10 years. And the highest-performing mutual fund in my portfolio has generated a 21.9% return over the last 8 years.

So comparing mutual fund returns with PPF or any other fixed-interest product is not logically correct.

Flat Markets Test Patience, Not Intelligence

As I have mentioned in my earlier posts, I have been investing since 2010. This means I have seen the market’s ups and downs for more than a decade.

One important lesson I have learned is that flat markets test our patience, not our intelligence.

And if you manage to stay invested through such phases, markets often reward you significantly later.

In my experience, flat or sideways markets give tremendous opportunities to accumulate more units at lower prices, which helps investors benefit when the market eventually moves up.

So if you ever feel that your portfolio is not giving returns higher than your uncle’s FD, pause for a moment and compare long-term market returns with long-term FD returns.

You may often see headlines in big newspapers praising ULIPs or insurance products and claiming they beat equity returns in such times. But please don’t make the mistake of mixing insurance with investment.

I have already shared my ULIP mistake in detail in a separate article, which you can refer to.

The difference in long-term returns clearly shows why patience matters. During such phases, I often invest more—and this strategy has consistently rewarded me.

What Actually Went Through My Mind During This Phase

Nothing much came to my mind. It looked very normal to me.

I would not like to exaggerate this reaction, but it comes from my experience of nearly 15 years in equity markets and mutual funds.

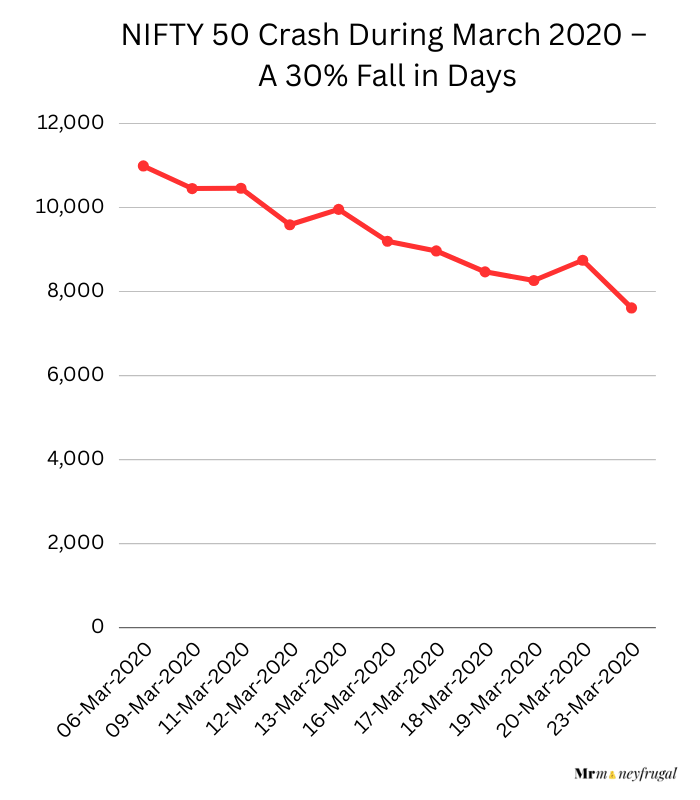

I have seen markets go up and go down— in fact, I have seen markets fall more than 30% in a single month, like during COVID-19, for which I will share a detailed post separately.

Between 6 March and 23 March 2020, NIFTY 50 fell nearly 30%. Investors who panicked locked in losses. Investors who stayed invested saw strong recovery later.

However, new investors may not feel comfortable with such returns.

Also, the media and newspapers often narrate such stories very loudly, which can make new investors panic and end up doing the wrong things with their portfolios.

But if you are investing for the long term—which you should be when investing in equity products— and if you have done your homework properly by researching funds before investing, This is actually the time to relax and do nothing.

")

After falling nearly 30% between 6 March and 23 March 2020, NIFTY 50 recovered strongly and ended the year higher than its pre-crash level. Short-term volatility did not define long-term outcome.

What New Investors Could Do in Such Times

When I started investing, I used to look at NAVs daily and track my portfolio multiple times a day. Seeing my portfolio not generating returns better than safe products was something I did not like at all.

But because I was reading a lot and learning continuously, I did not take any action. Instead, I kept investing and gradually increased my investments.

New investors, however, if they are not well-informed, may feel tempted to quit— which they should avoid in every possible way.

Inaction Is the Only Way Out in Such Times

The best thing you can do during such phases is actually to do nothing. And the reason is simple—you are not doing anything wrong.

This is just a phase, and like every other phase in the market, it eventually changes.

So neither switch nor sell—just do nothing.

Today, I can proudly say that whatever I have earned through investing has come not from doing too many smart things, but from avoiding stupid mistakes.

The Hidden Job of SIPs During Boring Markets

The biggest benefit of investing through SIPs is rupee cost averaging.

And during flat markets—which often feel boring because of the dullness all around—you get the maximum benefit of it.

You simply accumulate more units of the same scheme at similar or lower prices. So, in reality, you are in an accumulation phase.

Since SIPs make investing easy—because you don’t need to transact manually and everything happens automatically— you should ideally forget about the market and come back when things start looking more exciting.

Why Consistency Matters in Flat Markets

In the market, there are two things that can make you a long-term winner.

First is doing your research properly before investing. Second is staying patient when things appear to not go as per your expectations.

I strongly believe that anyone who follows these two principles can outperform nearly 90% of novice investors in the market.

The reason is simple: most people hardly do any research before investing and instead rely on tips and recommendations from others, and very few people have the patience to stay invested during dull phases.

So let your SIPs continue. The reward of consistency may surprise you.

The Lesson New Investors Usually Learn Too Late

New investors want to see results fast. They often assume that markets are bound to give higher returns just because they expect them to.

I had similar thoughts when I started investing.

I wanted to get rich quickly. Back then, I didn’t fully understand that even a 12% CAGR sustained over 20+ years can create significant wealth.

You can too calculate through our SIP calculator and learn how small investment can yield big wealth in time.

Instead, I wanted my money to double every year.

This mindset is exactly why many new investors panic during temporary losses and end up selling.

And this is one of the main reasons why most SIPs fail—because investors quit too early.

What I Would Do Differently If I Were Starting Again

As I have already mentioned in this post, I used to check NAVs daily when I started investing. That is something I would not do again.

Instead, I would focus on learning more, reading consistently, practicing patience, finding the right mentors, and staying disciplined and consistent to reap the maximum benefits from my investments.

And if you want to learn more about mutual funds, you can check out our detailed mutual fund learning platform, which covers 100+ basic questions and answers on mutual funds to help you easily learn and understand how mutual fund investing works.

If you are also interested in investing in new companies raising funds through IPOs, you can visit our IPO calendar page, which lists all upcoming and live IPOs in one place.

You can read detailed information about each IPO to make better and more informed investment decisions.

FAQ:

Should I stop my SIP if returns stay low for 1–2 years?

No, you should not stop your SIP if returns stay low for 1–2 years. In the short term, market volatility can lead to low or flat returns. You should give a mutual fund at least 3–5 years to properly evaluate its performance and see whether it is performing in line with its peers and benchmark.

How long is ‘long term’ actually?

There is no fixed definition of “long term.” It could be 5 years for someone and 30 years for someone else, depending on goals and time horizon. However, generally speaking, 10+ years is often considered long term when it comes to SIPs and equity investing. This is how I personally look at long-term investing.

What if my SIP underperforms even after many years?

If your SIP underperforms for many years without any clear reason such as broad market volatility, and peer funds are performing better, you should analyze your fund more closely. However, do not make any decision in a hurry.

If peers have been consistently doing well in the same market for 3+ years, then you may consider planning an exit, but only after thorough analysis.

Is SIP still worth it during sideways markets?

Yes, in fact, sideways markets can be good for investing through SIPs because you are able to accumulate more units at lower prices. When the market eventually moves up, the value of these accumulated units can increase.